Life is like a road. There are long and short roads; smooth and rough roads; windy and straight roads. Many roads are on the map as we journey through life. There are roads that lead to a life of marriage and family or others that lead to a fulfilling career with or without a family. There are roads that lead to fame and fortune on one hand or isolation and poverty on the other. There are roads to happiness as there are roads to sadness, roads towards victory and success, and roads leading to defeat and disappointment.

Just like any road, there are corners, detours, and crossroads in life. Perhaps the most perplexing road that you would encounter is an intersection. With four roads to choose from and with limited knowledge of where they would go, which road will you take? What is the guarantee that you will choose the right one? Will you take any road, or just stay where you are: in front of a crossroad?

Guess what-There are no guarantees!

You do not really know where a road will lead you until you take it. There are no guarantees. This is one of the most important things you need to realise about life. Choosing to do the right thing ( what even is the “right” thing) all the time would always lead you to happiness. Loving someone with all your heart does not guarantee that it would be returned. Certainly, fame and fortune do not guarantee happiness. Fast tracking your way up the corporate ladder by accepting a “favour” from somebody is not always bad, especially if you are highly qualified and competent. There are too many possible outcomes, which you really cannot control. The only thing you have power over is the decisions that you will make, and how you would act and react to different situations.

Wrong decisions are always far clearer in hindsight.

Had you known that you were making a wrong decision, would you have gone along with it? Perhaps not, why would you choose a certain path when you know it would get you lost? Why make a certain decision if you knew from the very beginning that it is not the right one? It is only after you have made a decision and reflected on it that you realise its relevance. If the consequences or outcomes are good for you, then you have decided correctly. Otherwise, your decision was wrong, but even a seemingly “bad” decision can produce some positive benefits. Taking the wrong path might turn into “the scenic route” where you discover new things. That bad career move might have given you a skill that you would not have otherwise achieved, or maybe a bad relationship created beautiful children that you cherish.

Take the risk: decide.

Since life offers no guarantee and you will never know that your decision would be wrong until you have made it, then you might as well take the educated risk and decide. It is definitely better than keeping yourself stuck in a rut complaining that nothing ever goes right, or dreaming that “one day life will change”. Although it is true that one wrong turn could get you lost, it could also be that such a turn could be an opportunity for an adventure, as you discover more roads. It is all a matter of perspective. You have the choice between being a lost aimless traveller or an accidental tourist of life. But take caution that you do not make decisions haphazardly. Taking risks is not about being careless and stupid. Here are some pointers that could help you choose the best option in the face of life’s crossroads:

· Get as much information as you can about your situation.

You cannot find the confidence to decide when you know so little about what you are faced with. Just like any news reporter, ask the 5 W’s: what, who, when, where, and why. What is the situation? Who are the people involved? When did this happen? Where is this leading? Why are you in this situation? These are just some of the possible questions to ask to know more about your situation. This is important. Oftentimes, the reason for indecision is the lack of information about a situation.

· Identify and create options.

What options do the situation give you? Sometimes the options are few, but sometimes they are numerous. But what do you do when you think that the situation offers no options? This is the time that you create your own. Make your creative mind work. From the most simplistic to the most complicated, entertain all ideas. Do not shoot anything down when an idea comes to your head. Sometimes the most outrageous idea could prove to be the right one in the end. You can ask a friend to help you identify options and even make more options if you encounter some difficulty, but make sure that you make the decision yourself in the end. Remember there is rarely only one road to any given destination.

Consider this scenario. You wish to travel from Brisbane to Sydney – you have no time restraints to arrival time. Will you fly? Will you take a coach? Will you drive? Which highway will you take? There are many options, but in the end, all will see you arrive at your destination. Are any one of these paths “wrong?”

· Weigh the pros and cons of every option.

Assess each option by looking at the advantages and disadvantages it offers you. In this way, you get more insights into the consequences of such an option.

· Trust yourself and make that decision.

Now that you have assessed your options, it is now time to trust yourself. Remember that there are no guarantees and wrong decisions are always in hindsight. So choose… decide… believe that you are choosing the best option at this point in time.

Now that you have made a decision, be ready to face its consequences: good and bad. It may take you to a place of promise or to a land of problems. But the important thing is that you have chosen to live your life instead of remaining a bystander or a passive onlooker of your own life. Whether it is the right decision or not, only time can tell. But do not regret it whatever the outcome. Instead, learn from it and remember that you always have the chance to make better decisions in the future.

· Take action and make the move.

The next step in making the decision is to take ACTION. After all, it is no good if you are at the intersection, with the brakes on and you decide to go right and do not move your foot to the accelerator. Without action, you will remain right where you are – good or bad decisions.

On my path in life, I am aiming to create a 10/10 life for myself in all areas. And you can too,

discover your path at risetorich.net

As I read blogs and self help books, I am always amazed at some of the true Rags to Riches stories that abound.

While I have never earned a huge salary, been unemployed for any long period of time or been even close to homeless, I have not often ever thought of my situation as being POOR.

Except for ONE DAY. Let me tell you about it.

The year was 1984, I had been working as a photographic assistant in an advertising agency in the city.

For a young 20 year old girl who was newly married, it was a glamorous position. It was very “Mad Men” with the ad execs ( both men and women) in suits, champagne lunches and celebrity “talent” often arriving in the office.

One of my duties at this job was relief receptionist to cover the lunch hour. I enjoyed this and was paid a small bonus for the extra work. All was going well, I loved the people and the job…UNTIL… I fell pregnant. Sadly 1984 did not have the equality of workplaces today and I was told that it was “not a good look” to have me in the office 🙁

I did manage to find another job from a friend and I was able to work a couple of days a week while some staff members were on holiday.

My husband was working full time and we actually got along reasonably well on the reduced wages. I had been planning on having to reduce our budget to one wage anyway in preparation for the baby’s arrival.

Hubby had found a new job at a large factory nearby, we had a decent car and very little debt. Things were looking good. 🙂 UNTIL.

One Friday hubby came home and said that the factory he worked for closed down over the Christmas break for 4 weeks!! As he had not been there very long, there would be no wages for that time. A Trip to Social Security to see if we were eligible for any assistance proved fruitless. Because he technically still had a job, we were not able to access any benefits. We knew if he quit that job, the likelihood of getting it back in January was slim at best.

So, together we looked at what we had left and formulated a plan. We would need to cover the 4 weeks of close down plus the one week when he went back to work before the first payday.

We could see we just did not have enough… So we moved from the house we were into a tiny one-bedroom flat, we back traded the car to a “sort of” ok one and we felt we were ok. We now had no debt, I paid rent upfront for the duration of the time we would need. All we needed was food, petrol and utilities money.

For Christmas that year, we asked for baby stuff and cash and we were looking OK. We gave family and friends Christmas gifts that I had bought throughout the year, nobody missed out, and I did not need to break the budget. We even managed to have a couple of weekends away camping with friends over the Christmas break.

On Friday the 18th of January 1985, the last Friday before hubby was due to go back to work. Hubby filled up the car with petrol so he could get to work for the upcoming week and I went shopping with our last $20.

Keeping a couple of dollars aside for fresh milk and bread through the week, I spent that last few dollars on eggs, cheese, mince, onions, frozen mixed vegetables and some potatoes.

The resulting huge pot of mince, onions and vegies would turn into the following meal plan for that week :

Savoury Mince on toast x 2

Add some tomato paste and pasta from the pantry and have (sort of ) spaghetti bolognese x 2

Add some mashed potato and grated cheese on top and call it shepherds pie x 2

Add some to roast jacket potatoes

And for the last night whatever was left over could get a tin of tomatoes and some pasta added and it turned into “minestrone”

We were quite proud of ourselves for managing so well at such a tough time. We had not asked family for any money at all, and I doubt they knew we were as skint as we were.

It was a stinking hot Brisbane day, so after dropping me back at the flat with the shopping, hubby and his friend were going out to Centenary Pool in Brisbane (about 20 minutes away from where we lived on the North side) to have a “play” They have high diving towers that “boys” like jumping off 🙂 I set about preparing the big stock pot with the mince mixture and by the time it was simmering away, I was sitting down watching TV.

The first indication that we may have had a problem that day, was it started raining. Then it rained HARDER, then the wind started. The wind was so ferocious I could see the glass sliding door bowing under the force. Then the hail began. At that point I got scared. 🙁 I was 8 months pregnant, on my own in a TINY flat with nowhere to go that felt safe.

Hubby and his friend had seen the storm coming from the high tower of the pool and had started heading home they made it roughly halfway when they got stuck in the hail. From their accounts, the hail was horizontal as it slammed through the back windscreen and broke the front. They were both huddled under the thick car seat covers of our friend’s car.

When they were able, they tried to make it home and they both said that when they came closer to our suburb they were both really scared for both their wives. It looked like a bomb zone.

When hubby got home, he called out for me as he could not find me. When I heard him, I called out and he found me in a curled-up mess hiding in the bottom of the tiny linen cupboard/broom cupboard in the flat. It had not been a fun afternoon 🙁

Our flat was totally devastated with not one single window left whole. The place was flooded the carpet was ruined, the curtains shredded and our bed was also soaked. When I had a look in the kitchen, that is when it hit me the hardest, my big pot of food for the ENTIRE WEEK had broken glass all through it.

There was no power or phone as the lines were all down. We could not contact anybody to see if they were ok. On the way back from town, Hubby had come through the suburb where my parents lived and said it was very badly damaged there too, but we had no way of knowing if we would be able to go there and the reports we were hearing on the radio in the car suggested we would not be able to get through. The inlaws lived approximately 50kms north and it was getting dark by this stage, so there was not much we could do but put a tarp on the floor to try and stay dry, blow up our camp mattress and attempt to get some sleep.

I remember we had sandwiches for dinner that night.

The next morning we were able to get a look at the damage. What a mess. Still no power. ( it would take a couple of days to come back on) and of course NO FOOD 🙁

This was absolutely the lowest point of my life. I honestly had NO IDEA what we were going to do.

Later that day, our landlord came to see the block of flats ( he owned the whole block) He said we could not stay there and gave us $50 in cash to help out until he could get the glass doors and carpets replaced. He also offered that we would have free rent for the time we were not able to live in the flat.

Not long after the landlord had been, hubby’s Mum came. We packed up what we could and spent the next couple of weeks at her house, before finally returning to a fully renovated flat.

It was quite some time before I could face the thought of making Savoury Mince 🙂

OH NO!! you might be thinking that this is yet ANOTHER New Years Resolution post. It is not!!

In fact I don’t “do” resolutions. As most of you know, resolutions are easily made, but seldom kept, with most being broken by the first week in January.

What I DO do, is have a strategic plan for my year. This is broken down to a Quarterly Plan, Monthly Plan and finally Daily Tasks. That is not to say that I am so scheduled that there is no room for spontaneity and fun. My daily tasks are flexible enough to cope with almost any diversion without causing the whole plan to implode.

So how to start?

To move forward, you first need to know where you are right now. Take a good hard look at the state of your life and decide – REALLY decide to move each area just one step closer to your version of perfect.

Now the point here is to look at YOUR version of perfect. The perfect holiday for instance for me is not a 5 star hotel, but rather a cute cottage by the beach or in the country that is close to a farmers market where hubby and I can buy some amazing local produce and spend a lazy afternoon cooking up a superb meal.

To help guide you to see where you are right now, and them move forward, why not take a look at my “Getting $#!T Done” course

Does that number strike a feeling of panic and dread, or are you ready for the holiday season?

I have to admit, I am one of “those” annoying people who does not stress about Christmas or the cost of giving gifts. And, yes, I have just about finished my Christmas Gift shopping.

Why?? Well because I buy all throughout the year 🙂

I am fairly lucky in the fact that we do not have a huge family so I only need to buy around 20 gifts.

My husband knows that I cannot pass by a sale table or dump bin 🙂 Invariably I see something and think “Oh! “S” would like that” or “Wow! That would be great for “M”

I have one shelf in a cupboard that we call the “present cupboard” On the inside of the cupboard door is a small whiteboard with all the names written down one side in permanent marker.

Then I fill in the gifts as I buy them in whiteboard marker. That way it is a simple matter to erase the gifts as they get given.

I also know that some of the best gifts can be bought at a bargain price at certain times of the year.

Anything “Christmas-y” can be bought for a tiny fraction of the price just after Christmas. I always buy Christmas paper and cards in the last week of December, often at up to 90% off. Look for such items as paper, cards, decorations for the tree, and themed tableware like plates, bowls, glasses etc. I like to have a supply of Christmas theme plates, cups or glasses that I can use as part of a gift. Make a cake or batch of cookies and display them on a Christmas plate, or simply place chocolates into a Christmas mug and wrap them with cellophane.

The lead-up to New Year’s Eve often brings up good specials on Champagne, Wine and other Alcohol. It can be a good time to buy for birthdays early in the year.

January is the best time to buy stationary, school supplies and office equipment in the “back to school” sales. This is a good time to buy plain-coloured kid’s clothing and running shoes.

February is the time to buy chocolates in the after Valentine’s Day sales.

March -April is Easter, and again after Easter is the time for chocolate and “Easter-y” decorations.

May is Mother’s Day. This is a good time to pick up perfumes, bath sets, soaps, and kitchen appliances.

June – July is a time to keep an eye out for End of Financial Year Sales. This is often the best time to buy big appliances or cars. Any big ticket items often have sales targets to reach and you can very often drive a hard bargain the closer it gets to June 30. Also at this time of year, the Christmas Toy Sales start with the option to purchase on a 6-month lay-by.

August is usually quiet with no major sales happening.

September is Father’s Day and Football grand finals. Father’s Day is a time to pick up gift sets of male toiletries, hardware, BBQ accessories and food sets ( think BBQ sauces and rubs etc), tools, car-related things and the ubiquitous alcohol.

The last weeks of September are another time to stock up on alcohol as the stores prepare for football grand final parties.

October is the Bathurst Car Race weekend, so again there are car-related accessories on sale.

November- December brings sales in the lead-up to Christmas.

I find that by purchasing gifts throughout the year, the strain on the budget is minimal. Our family has a dollar figure to work to for gift giving, so I can regularly spend the recommended amount but give a much higher value gift – eg a $50 gift budget, can result in a $100 value when that gift is bought at 50% off.

Did you read my recent post on what “they” say is the amount of money needed to retire? (it is here)

When this was originally reported, I said to my husband, “I am sure we could live on the pension as well as Mum & Dad.”

So, we decided to try it. Before making any sort of budget, I tracked our spending for 3 months to see exactly what we were spending, it was surprisingly low.

For our “live on the pension plan” we have not taken into consideration our mortgage or my husband’s car. We are working on the assumption that, like our parents, our home will be fully paid off and we will have just one car, which we will have no debt on, but will need funds to update regularly.

Every week I allocate the correct amount of cash for our budget needs within the confines of only having the amount for the current aged pension for a couple to live on. Bills are direct deposited to their relevant accounts (eg: I send $50 per week to our council for Rates, $50 a week to the Power company etc)

We have lived this way for the past 3 years or so and have not felt we have missed out on much at all. By not spending, we have seen a huge reduction in our debts. (BONUS)

This has spurred us on further to keep going with “living on the pension” for the next few years. We are aiming to be completely debt free in the next 2 years and then sell our businesses and be able to retire early. This of course will require a fairly decent amount of money in the bank, as we are both quite a way off being able to receive the actual pension.

My life of living a “Champagne Life on a (lite) Beer Budget” has been heavily worked with this way of living. Both my husband and I have our own businesses and they both do very well. From the outside, it appears we might splash the cash around quite readily, but in reality, we live within our “pension” budget.

I drive a new BMW which my business provides the funds for, there is money put aside in the “pension” budget to upgrade the car. Hubby’s business has work utes that we do not spend a lot on, as they are – well – work utes!

We plan on updating the BMW as often as we can well into retirement. We have found that the price of updating while the car has low mileage and is reasonably “new” is quite affordable and within our budget, especially when spread out over 3 years or so.

I love to travel, but our businesses are such that we can really only get away for the odd weekend, Easter and Christmas. I often find great deals for weekends away on daily deals sites that allow us to get away at a reasonable price. I also keep an eye on the airline deals and have been able to snag great deals on flights.

We both enjoy eating out and have a subscription to the Entertainment book each year. Using the vouchers, we can eat at more expensive restaurants than we would normally for half price. We also enjoy cooking, looking at restaurant menus and cooking similar meals at home for a fraction of the cost makes for an afternoon of culinary fun at home. A well stocked pantry and a good bulk butcher nearby, keep our grocery budget at a manageable level. It is the “grocery” section of the budget that I often find has a built-up surplus. This surplus gets either transferred to savings or put aside for meals out.

Like our parents, we do not “need” anything, so when asked what we want for a gift on birthday and Christmas, I often ask for experience type gifts. Vouchers for cafes, spa treatments etc are happily accepted.

The lessons we have learned from living within the pension amount is that, for us, it is achievable without any huge sacrifices. Our budget does not include any pension discounts from expenses such as utilities, registration, rates etc, so those will be bonuses if we receive them. We are blessed with good health and are conscious that chronic illness which requires long periods of expensive medications would be a burden on the budget.

Why not look at your own budget and decide if you could live on the pension?

Quite some time ago I read a news report debating whether or not the Australian aged pension is “enough” to live on in today’s economy.

As expected, the comments were mixed with a lot of people saying they can NOT live on the amount received from the government.

(I must admit, I do find it amazing when I see these types of reports where we see a woman complaining that she does not have enough money for electricity to keep warm, but she is being interviewed in a thin cotton top. – Put a jumper on!!)

Both my parents and my in-laws are retired, and I have seen them live a happy and activity filled retirement over the last 15-20 years. They are not having any trouble at all living successfully on the pension. My parents are in between the “modest” and “comfortable” categories and just simply cannot spend it all. In-laws are on the aged pension only and live as well as we do, if not more socially. My Father recently passed away and Mum is now on a single pension with a small superannuation top up, and still, the bank account keeps rising.

The number one thing I have noticed that has led to living comfortably on the pension is to own the roof over your head. Most reports show that housing is the number one cost for retirees. Retiring with no debt, a small nest egg and a low maintenance home has shown itself to be a huge benefit to both sets of parents.

Also, retirement is not all about how much money you have. How many of us “young’uns” just wish for time to do what we want? Retirees will often say, they don’t know how they had time to work. Gardening, craft, and reading a good book or magazine are things that often get somewhat neglected in the hustle and bustle of a busy working life.

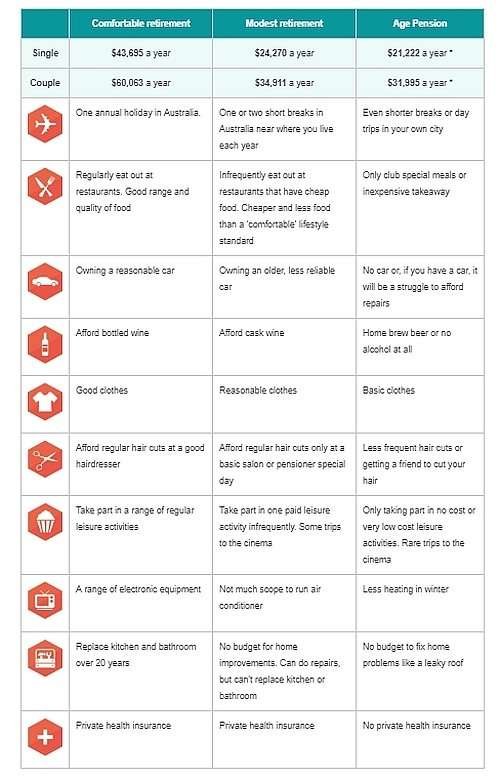

This table proposes the amounts supposedly needed for varying levels of retirement.

One thing that the “gurus” neglect to think of is peer groups.

If retirees are surrounded by other high income retirees who travel overseas often then yes, they may need a much higher figure.

My parents were in a caravan club so they travelled quite extensively. They are not interested in international travel (apart from NZ where we have some family – does NZ even count as international???)

The in-laws love train travel and have done the Spirit of the Outback a few times We looked at doing the Outback with them one trip but without the pensioner discount it is REALLY expensive.

Both parents eat out ALL THE TIME. We regularly get an answering machine because they are out to dinner. Usually clubs, but certainly not restricted to the “seniors specials”, because that is what they like to eat. None of them are into “towers of no food” as my Dad called “better” restaurants.

Both Mothers have overflowing pantries that we joke will feed us for years when we eventually have to clean out the houses. Regular catch ups with friends over a new cake or biscuit recipe and a cuppa are commonplace.

Both parents have always had late model cars that are regularly maintained. Because of the van, Dad had a fairly new 4×4, and since his passing, this has been sold. Mum does not drive so that vehicle expense is now partly taken up with community bus fares. The in-laws have not long upgraded their car to a late model small 4cyl Toyota.

All drink bottled wine bought beer, spirits, sherry and port.

Clothes, the men are men and don’t really care. The Mums just buy clothes and they wear them. The Mothers are both well dressed from Rockmans, Millers, Noni B etc so reasonable clothes. (Although neither woman was a “designer clothes” wearer)

All get their hair cut at local hairdressers and look neat and tidy at all times.

As mentioned previously, they have active social lives filled with leisure activities. Cinema outings, meals with friends and craft group outings feature regularly on the calendar.

The houses are both fully owned, modern homes that are standard 4/2/2 and are in good condition. Neither house will need new kitchens or bathrooms in their lifetime.

Neither have health insurance and have not needed it. There has been some serious illness (1 cancer, 2 diabetics, 1 aortic aneurism op) and of course, all have glasses. The public system has been FANTASTIC and none of us can complain about the quality or timeliness of treatment. In the last year of Dad’s life, he had multiple trips to the hospital and weekly visits to his GP, all in the public system. Nothing could have been done any differently in the Private system to make his last year any different.

Watching our parents age has been a wonderful learning experience for my husband and I. We are not worried about our level of comfort in retirement at all. We are working on setting ourselves up now, and look forward to our golden years.

Many of us have been raised with the idea of "saving for a rainy day", so we diligently squirrel away savings for a disastrous event.

While it is important to have a safety net backup, "Sunshine Cash" is the complete opposite :) It is the money to have FUN with, money to burn, money to enjoy, and money to LIVE.

It is the formula that has seen me "Rise to Rich" and I can help you do the same.

Where to now? Join me on the Sunshine Cash journey. Follow me on Facebook, Pinterest and Instagram for tips and hacks to create YOUR best life.

Oh! Please do comment on my posts. I love to know if something resonates with you, or how you do things differently. I love to hear your stories.

Since life offers no guarantee and you will never know that your decision would be wrong until you have made it, then you might as well take the educated risk and decide. It is definitely better than keeping yourself stuck in a rut complaining that nothing ever goes right, or dreaming that “one day life will change”. Although it is true that one wrong turn could get you lost, it could also be that such a turn could be an opportunity for an adventure, as you discover more roads. It is all a matter of perspective. You have the choice between being a lost aimless traveller or an accidental tourist of life. But take caution that you do not make decisions haphazardly. Taking risks is not about being careless and stupid. Here are some pointers that could help you choose the best option in the face of life’s crossroads:

Since life offers no guarantee and you will never know that your decision would be wrong until you have made it, then you might as well take the educated risk and decide. It is definitely better than keeping yourself stuck in a rut complaining that nothing ever goes right, or dreaming that “one day life will change”. Although it is true that one wrong turn could get you lost, it could also be that such a turn could be an opportunity for an adventure, as you discover more roads. It is all a matter of perspective. You have the choice between being a lost aimless traveller or an accidental tourist of life. But take caution that you do not make decisions haphazardly. Taking risks is not about being careless and stupid. Here are some pointers that could help you choose the best option in the face of life’s crossroads:

Does that number strike a feeling of panic and dread, or are you ready for the holiday season?

Does that number strike a feeling of panic and dread, or are you ready for the holiday season?

Did you read my recent post on what “they” say is the amount of money needed to retire? (

Did you read my recent post on what “they” say is the amount of money needed to retire? (

Quite some time ago I read a news report debating whether or not the Australian aged pension is “enough” to live on in today’s economy.

As expected, the comments were mixed with a lot of people saying they can NOT live on the amount received from the government.

(I must admit, I do find it amazing when I see these types of reports where we see a woman complaining that she does not have enough money for electricity to keep warm, but she is being interviewed in a thin cotton top. – Put a jumper on!!)

Both my parents and my in-laws are retired, and I have seen them live a happy and activity filled retirement over the last 15-20 years. They are not having any trouble at all living successfully on the pension. My parents are in between the “modest” and “comfortable” categories and just simply cannot spend it all. In-laws are on the aged pension only and live as well as we do, if not more socially. My Father recently passed away and Mum is now on a single pension with a small superannuation top up, and still, the bank account keeps rising.

The number one thing I have noticed that has led to living comfortably on the pension is to own the roof over your head. Most reports show that housing is the number one cost for retirees. Retiring with no debt, a small nest egg and a low maintenance home has shown itself to be a huge benefit to both sets of parents.

Also, retirement is not all about how much money you have. How many of us “young’uns” just wish for time to do what we want? Retirees will often say, they don’t know how they had time to work. Gardening, craft, and reading a good book or magazine are things that often get somewhat neglected in the hustle and bustle of a busy working life.

Quite some time ago I read a news report debating whether or not the Australian aged pension is “enough” to live on in today’s economy.

As expected, the comments were mixed with a lot of people saying they can NOT live on the amount received from the government.

(I must admit, I do find it amazing when I see these types of reports where we see a woman complaining that she does not have enough money for electricity to keep warm, but she is being interviewed in a thin cotton top. – Put a jumper on!!)

Both my parents and my in-laws are retired, and I have seen them live a happy and activity filled retirement over the last 15-20 years. They are not having any trouble at all living successfully on the pension. My parents are in between the “modest” and “comfortable” categories and just simply cannot spend it all. In-laws are on the aged pension only and live as well as we do, if not more socially. My Father recently passed away and Mum is now on a single pension with a small superannuation top up, and still, the bank account keeps rising.

The number one thing I have noticed that has led to living comfortably on the pension is to own the roof over your head. Most reports show that housing is the number one cost for retirees. Retiring with no debt, a small nest egg and a low maintenance home has shown itself to be a huge benefit to both sets of parents.

Also, retirement is not all about how much money you have. How many of us “young’uns” just wish for time to do what we want? Retirees will often say, they don’t know how they had time to work. Gardening, craft, and reading a good book or magazine are things that often get somewhat neglected in the hustle and bustle of a busy working life.

This table proposes the amounts supposedly needed for varying levels of retirement.

This table proposes the amounts supposedly needed for varying levels of retirement.